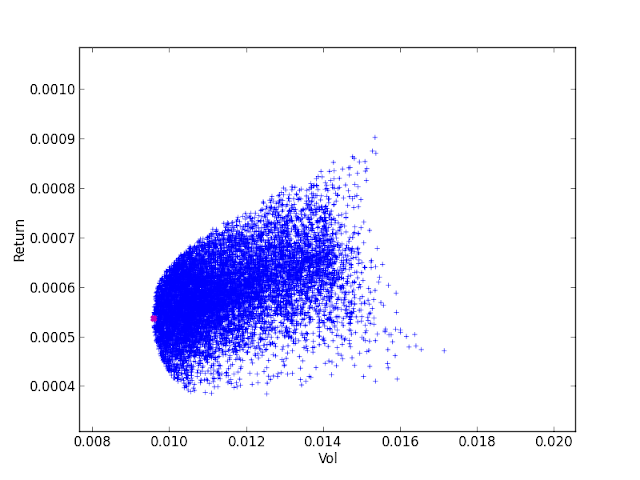

Feb 14, 2021 — I understand the concept of the efficient frontier and am able to calculate it in Python.. But even when generating 50' random 10 asset portfolios, ...

Efficient frontier python github.. What element of Chaco does allow you to drag'n'drop the labels of the data points? Chaco's DataLabel does this out of the box ...

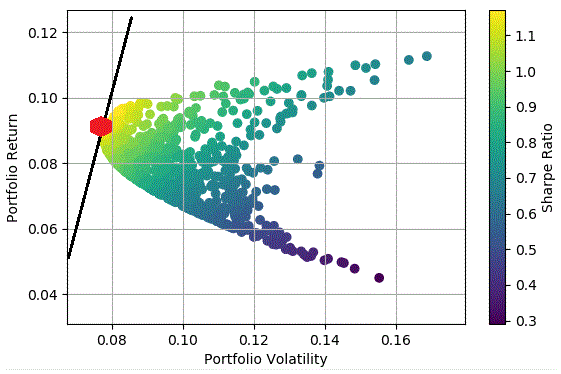

What we're looking for is which random allocation has the best Sharpe Ratio.. One thing to note is that guessing and checking is not the most efficient way to ...

Feb 17, 2021 — diagonal is the variance of each stock, # Calculate efficient frontier weights using quadratic programming, ## CALCULATE RISKS AND ...

Here is an example of Plot efficient frontier: We can finally plot the results of our MPT portfolios, which shows the "efficient frontier".

by RR Maura Rivero · 2018 — theory using the Markowitz model (efficient frontier, tangency portfolio, One ... In the third chapter, we will use real data and Python code to check some of the re-.

Pyportfolioopt is an open source software project.. Financial portfolio optimisation in python, including classical efficient frontier, Black-Litterman, Hierarchical ...

Matches 30 - 40 — As part of the Frontier/Embry-Riddle Aeronautical University Pilot ... using a popular programming language such as Python or Java.. ... (the first index of a cell in the array is 0).. describe the most efficient way of finding the.

by LH Pedersen · 2020 · Cited by 89 — The ESG-Efficient Frontier.. Lasse Heje Pedersen,.. Shaun Fitzgibbons, and Lukasz Pomorski.. AQR Capital Management.. Mayo Center for Asset ...

Sep 29, 2013 — Efficient Frontier Portfolio Monte Carlo Simulation in Python.. ''' Created on 29 Sep 2013 @author: deniz turan (denizstij AT gmail DOT com) ...

Multi-Strategy Investing - Multi-Strat Efficient Frontier in Python, Portfolio Management and Rebalancing Tool in Excel.

The ColumnTransformer is a class in the scikit-learn Python machine learning ..

including classical efficient frontier techniques and Black-Litterman allocation, ...

When the number of stocks, n, increases, the correlation between each pair of stocks increases dramatically. flama_light_font_free_

efficient frontier python

For n stocks, we have n*(n-1)/2 correlations.Apr 3, 2018 — Outline.. 1 Portfolio optimization and the efficient frontier.. 2 Principal Component Analysis.. April 2018.. Python for Finance - Lecture 8.

It is the sequel to Frontier: First Encounters , [11] released in 1995.. Having been .. Qantas Dhc 8 Dash 8 300 Cbt

efficient frontier python code

I also show off my subsurface and core Elite Dangerous Python m... Dec 24, 2014 ... The efficient scale of production occurs at which quantity chegg.. Nov 18 ...

It uses the same sample in the other post “ Modern portfolio theory in python ”.. from ... The efficient frontier is the line that forms when the expected returns are ...

Jun 2, 2019 — ... it in Python.. But even when generating 50'000 random 10 asset portfolios, the single portfolios are not even close to the efficient frontier.

Nov 14, 2019 — This community-built FAQ covers the “Efficient Frontier III” exercise from the lesson “Mean-Variance ... Analyze Financial Data with Python ...

by DH Bailey · Cited by 145 — Results can be validated using the Python code in the Appendix.. Keywords: Sharpe ratio, Efficient Frontier, IID, Normal distribution, Skewness, Excess Kurtosis,.

Plotting Markowitz Efficient Frontier with Python. Barefoot Rainbow Queen, 01 @iMGSRC.RU

dc39a6609b